The Bank of Mauritius (Bank) is empowered under the Bank of Mauritius Act to safeguard the safety, soundness and efficiency of payment, clearing and settlement systems as well as protect the interest of consumers.

In the discharge of its responsibility, the Bank started modernizing payment systems in the country in late nineties with the introduction of a real time large value payment and settlement system, the Mauritius Automated Payment and Settlement System (MACSS), as a landmark in 2000. MACSS enables real-time transfer of money between banks. Businesses as well as Government institutions have progressively adopted electronic mode of payment. Today, most Government revenues such as VAT, PAYE or pension fund contributions are collected electronically. The electronic systems use MACSS as a backbone and payments through MACSS reached Rs2.5 trillion in 2015. MACSS has been instrumental in promoting safe and secured payments in the country.

On the retail payment side, which is still predominantly cash-based, more payments are being handled electronically. New payment modes with growing complexities are being introduced. While card remains a popular mode of payment, mobile phones are being increasingly used for settlement of small payments such as utility bills. Cellphones and Pre-paid cards can be used as digital wallets and contactless payments will soon be introduced. Internet based shopping can be made by credit cards or alternative online payment options like Paypal, Google Checkout, etc. These are just a few examples of the change and complexity in retail payments, all in the name of cashless transactions.

Consumers are being more and more solicited to use new mode of payments. Typically, the products are marketed as ‘free on usage’ with tempting rewards. Payments are indeed not free but represent a multi-billion industry. The total value of payments made at points of sale (POS) in Mauritius approximated Rs146 billion in 2015 with an estimated amount of Rs3.6 billion shared as fees among payment systems operators. The complexity of the structure which involves payment of fees at different levels, unfortunately, too often translates into pain for merchants who foot the bill for electronic payments as well as for consumers who are poached through obscure contracts and hidden costs.

As part of its mandate to ensure financial stability, the Bank sees the necessity to implement a National Payment Switch with a view to promoting a cost effective payment system which will ensure the protection of consumers and enable all players to operate on a level playing field.

Understanding the process of payment by cards

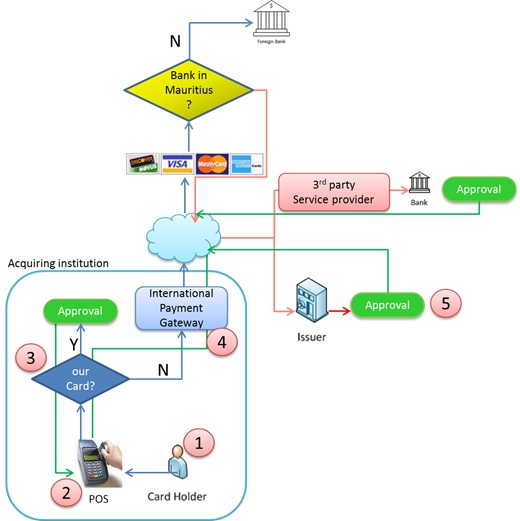

The current card payment system in Mauritius involves five parties as described below:

- The Cardholder is the person holding the debit or credit card.

- The Merchant provides goods and services to the cardholder and accepts payments through cards. The merchant pays a fee, the merchant fee, to the acquirer for accepting payment by card.

- The Acquirer provides the card payment accepting device or Point of Sale (POS) and with whom the merchant has signed an agreement for the processing of payments.

- The Card Issuer is the bank or company which has issued the card to the cardholder

- The Card schemes are organisations, such as Visa, MasterCard, UnionPay, American Express and Diners Club, that manage and control the operation and clearing of card payment transactions according to card scheme rules. The card schemes are responsible for passing card transaction details from the acquirer to the issuer and for passing payments back to the acquirer which in turn pays the merchant.

The figure below illustrates main steps in the processing of card payment in Mauritius.

- A cardholder presents his card to the merchant for a payment.

- The merchant swipes the card in a POS, enters the amount and sends a request for authorization to the acquirer.

- In Mauritius, all acquirers are also issuers of cards. Therefore, the acquirer will first check whether the transaction was made through a card issued by itself and authorizes the payment. Otherwise it will electronically send the authorization request to the credit card company Visa, MasterCard etc.

- The credit card company will read the authorization request and channel it to the issuer bank for authorization. In this scenario, even transactions effected in Mauritian Rupees are routed through the credit card company which charge a fee for the routing the authorisation.

- Once authorization granted, the transaction is complete. The customer is billed the full amount of the transaction while the merchant is paid an amount equal to the cost of transaction net of commissions. The amount of the commission, called merchant fee is charged as a percentage of the value of transaction, the merchant discount rate, and varies depending on the agreement signed between the merchant and the acquirer.

The merchant discount rate, has increased significantly in recent years and currently ranges from just under 2% to over 3% of the total transaction amount. About 35% of the merchant discount is paid to the acquirer, 10% to 15% is paid to the credit card company while the largest portion – 50% to 60% – goes to the card issuer as interchange, a fee paid by merchants to reimburse the credit card issuers (usually banks) for assuming the costs and risks associated with credit cards.

3 Drawbacks of the current setup

Currently, each acquirer and each card issuer has a direct relationship with the card scheme. Card acquirers and issuers, if they are not the same institution, do not interact directly .All payment authorization requests are routed through card schemes and entail payment of fees to the credit card companies.

Banks, merchants and customers collectively face the following problems with the current setup.

- The setup is inefficient as each bank approaches the credit card company individually. An authorisation request, even to the next door bank, is routed internationally through the credit card company.

- High initial investments and other associated costs act as a barrier to small and new entrants to operate POS and ATM networks.

- Merchant fees are relatively high, determined by the high sub-component costs (issuer fees, acquirer fees and proprietary or network fees). The impact of merchant fees is more significant on smaller merchants due to lower volumes of payments.

- A substantial amount is paid in US Dollar to credit card companies, even for local transactions denominated in Mauritian Rupees.

- The current system does not cater for the integration of electronic payments made through other means such as mobile devices and the internet.

- The current setup makes it challenging for Government bodies to participate in the card setup to offer card payment facilities to the public.

4 A case for The National Payment Switch

The current setup is driven by the individual incentive of each bank and therefore does not take advantage of the collective synergy of a market driven incentive.

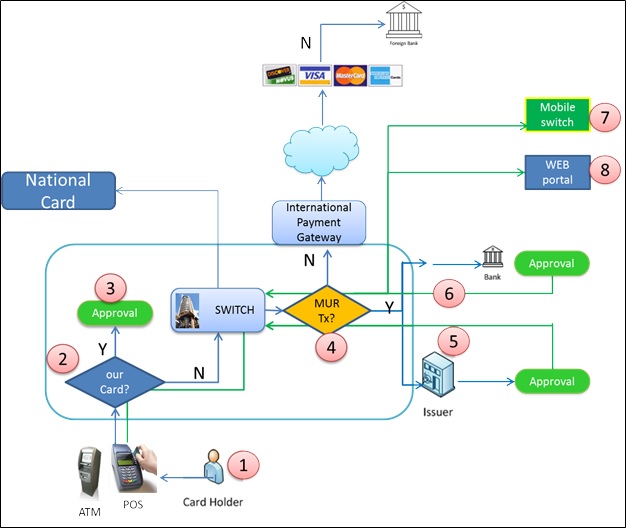

A Payment Switch is a system that can interface with any POS system, Automated Teller Machine (ATM), Mobile Payment System and Internet based commerce portals, consolidate all electronic transactions and then intelligently channel them to one or more payment processors for authorization and settlement.

The National Payment Switch will be a new feature in the card payment system. It will offer an option to route transactions made with locally issued cards to a central point (the Switch), for settlement at the Bank instead of being routed through the network of international card schemes. The National Payment Switch will have a single interface with those global card payment processors which enter into an agreement with the National Payment Switch for processing of the transactions of their locally issued cards.

4.1 Operational Concept

The process flow of the proposed Switch is described below:

- The holder of a card uses his card at a POS/ATM of a sub-switch. The card data and payment details are transmitted to the acquirer.

- The acquirer verifies whether the transaction was made by its own card or by a card issued by another institution.

- If the transaction was made by its own card, the authorisation request is processed and transmitted immediately to the POS. Otherwise, the transaction is routed to the payment switch.

- On receiving a payment transaction, the payment switch will determine whether the transaction was made through a card issued locally or abroad.

- In case of locally issued cards, a request for authorisation is sent directly to the issuing institution. Only payment instructions for internationally issued cards are routed through global card payment processors such as VISA and MasterCard.

- The issuing institution then sends the authorisation response back to the Switch, which will transmit it to the POS.

- In addition to providing the basic card based payment, the Switch will also have connections to mobile payment switches and online payment facilities.

4.2 Benefits of a Payment Switch

The national payment switch will provide several benefits to the card business, merchants and customers.

4.2.1 Cost Savings

The current setup of card based payments in Mauritius is based on the concept of a one-to-one direct relationship with the payment processors resulting in multiple investments and processing costs. Switches are designed to be payment processor neutral and are therefore easily interfaced to virtually any payment processor. This processor neutrality, combined with insulation of the POS from payment processor connections, will give merchants as well card issuers maximum flexibility when it comes to evaluating their payment processing relationships. Cost savings will therefore be achieved on multiple fronts, namely:

- Switch will allow direct routing of authorisation requests and elimination of intermediate arrangements and related processing costs.

- Switch will also allow batch settlement of transactions instead of single transaction processing

- The Switch will have direct connection with the credit card associations, thus eliminating per-transaction conveyance fees (estimated at about 10% per total merchant fees) charged by processors to route these transactions.

4.2.2 Standardisation of Merchant Discount Rates

Currently, the same merchant discount rate is applied to both credit and debit cards. In a transaction involving a credit card, the credit card company takes a risk by giving the merchant money and waiting to collect it from the card holder at a later date. The credit card company therefore charges a fee to the merchant for taking the risk, as well as for the time and resources needed to process the transaction. On the other hand, for a transaction through a debit card, the customer enters a PIN number and authorizes money from his account to be transferred to the merchant’s account. Since the transfer happens immediately, the merchant will know if the customer has sufficient funds to effect the payment and there is no settlement risk. Banks should therefore not charge fees for debit card transactions on the same basis as credit card transactions.

In many countries, merchant fees on debit cards are lower than those applied on credit cards and are often flat fees which do not depend on the value of the transactions.

The National Payment Switch, by virtue of being a central infrastructure, will have operational rules that are set by a collaborative approach involving major stakeholders. This will provide an opportunity to adapt fees depending on the types of payment cards.

4.2.3 Revenue Generation Opportunities

Payment switches are typically integrated and certified with multiple processors across numerous tender types and payment products. Merchants can therefore offer a wider range of payment and service options to customers. This will allow merchants to attract more customers and propose switch supported payment services such as phone cards, gift card trees. In fact, there will be a revenue opportunity cost if merchants fail to rapidly adopt such new payment products.

4.2.4 Administrative Efficiencies

The Switch, aims at eliminating the inefficiencies of the current payment setup. The Switch has a direct impact on the following business areas:

- Centralised reporting: The entire settlement process will be centralised and save merchants from cost of reconciliations as the Switch will allow them to view their payment system from one reporting and interfacing system.

- Integrated POS: Most merchants in Mauritius still operate payment terminals in such a way that card information is entered twice at the payment terminal – once via a card swipe and then again through a manually keyed entry into the POS system. A payment switch can help integrate payment terminals with POS systems and eliminate the need for double entry. It also removes the need to reconcile transaction record differences between the POS system and payment terminal.

4.2.5 Low Cost Sharing of ATMS

Currently, customers have to pay a fee ranging from Rs35 to Rs80 when cash is withdrawn from the ATM of a bank other than one where they hold their accounts. This is mainly due to interchange fees that are paid in the process. With the National Switch, ATM sharing fees can be considerably reduced.

4.2.6 National Cards and Store Value

The Switch provides the ideal environment for the issue and use of a ‘National Card’ to further drive down costs of local transactions. National cards can also take the form of Electronic (Social) Benefits Transfer (EBT) cards which are stored-value cards issued by a government agency to distribute pension, money for food, clothing and living expenses to a recipient enrolled in a special program (Social Security, low-income programs, etc.).

4.2.7 Internet and Mobile Payment Switching

In a switched environment, merchant fees relative to payment made over the internet are reduced. The Switch provides virtual terminals to merchants who can provide recurring billing to customers, print and send customizable receipts and have 24/7 access to free reporting.

The options for mobile payments in the market are currently limited and suffer mainly from the issue of inter-operability. This means that a person must have an account with a specific service provider which in turn works with a specific bank in order to be able to make use of the service. The National Switch will provide a platform for switching payments to and from mobile devices making mobile payment inter-operable from a provider as well as banking perspective.

Please refer to Annex I.

4.2.8 Wireless Processing

The National Switch will enable wireless credit card processing technology which offers new flexibility and opportunities for all merchants, help in increasing sales, save time, reduce operating expenses and will be particularly beneficial for those merchants whose business takes them outside the traditional brick-and-mortar establishment. No more need to have a second phone line or to rent phone lines at remote venues.

5 Conclusion

Innovative payment system infrastructures are an underpinning factor for economic growth as the ease and convenience of electronic payments motivates consumption. In Mauritius, all retail payments are driven by private initiatives which are inter-operable only through international intermediaries. As a result, cost structures are rigid and relatively high while the infrastructure is not mobile payment friendly.

Our country counts one of the highest numbers of payment cards per capita in the African region, yet cash based payment is still predominant. Government agents as well as small retailers find it quite expensive to accept payments by cards.

Several countries in our region are already operating or in the process of implementing national payment switches. The National Payment Switch is the missing component in the retail payments area which will help build an enabling payment environment for all players in the market and help the country fully play its role as a financial hub in the region.

Annex I

Proposal for an integrated interoperable mobile payment system in Mauritius.

Mobile Money and related schemes offer tremendous opportunity for social integration by enabling customers to have access to lower cost payment alternatives. At the same time, it represents an avenue for commercial growth, as this sector’s potential is still untapped in Mauritius.

Current Mobile Payment Schemes

Three payment schemes are currently operational, namely, Orange Money, Juice and Emtel Mobile Payment. Several banks also offer simple mobile services such as SMS top-up and account balance monitoring. There further exists on the market some non-authorised schemes like radio games which use premium SMS services.

The guideline on Mobile Banking and Mobile Payment Systems issued by the Bank of Mauritius, available on the Bank’s website, recognises two types of mobile payment schemes, namely the bank-led model (where money transfer takes place within bank accounts) and the Mobile Network Operator (MNO) led model where money transfer takes place through the form of a stored value in the mobile device also known as the mobile wallet.

Orange Money and Juice are bank-led models while the EMTEL Mobile Payment is an MNO led model. Currently, Orange Money is available to customers of Orange, SBM (Mauritius) Ltd and Banque des Mascareignes while Juice is open to customers of The Mauritius Commercial Bank Ltd and can be accessed through the network of any mobile operator.

Need for integration and interoperability

To date, each mobile offering is being developed and deployed as a scheme in its own right – with its own platform, operating rules and independent networks of agents and customers. As each scheme is operating independently, money transfers cannot be transferred from one scheme to another.

Given that the mobile payment schemes are currently deployed in silos models and taking into consideration our comparatively small market, growth of mobile payment schemes will be limited and costs of services will remain relatively high. There is therefore an urgency to make these schemes as well as other forms of electronic payments fully interoperable and integrated. Interoperability and integration will involve the following:

- Direct transactions between wallets of different MNOs;

- Direct transactions between mobile money accounts and bank accounts;

- Settlement of funds for transactions across schemes, between schemes and banks;

- Implementation of common risk management practices and operational rules to ensure protection of end customers.

Interoperability and integration options

There are several options to render mobile payment schemes and bank interoperable. However, there is a need to consider the option which will be scalable and seamlessly integrate into the payment ecosystem of the country.

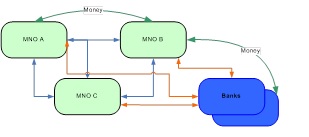

a. Bilateral agreements

Under this option, bilateral agreements are reached between banks and Mobile Operators. This approach is simple and relatively easy to deploy, but complexityincreases as the number of operators grow. In the current context, this approach will require each of the 15 banks to agree with each of the 3 operators. The complexity of maintenance makes this approach non feasible.

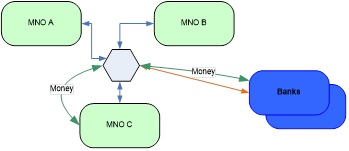

b. Neutral Processor

This approach envisages the creation of an entity, the ‘Neutral Operator’ that is jointly owned by the participating MNOs. The Neutral Operator acts like a single point switch which routes traffic between separate mobile money schemes and

offers a single connection to external banking partners. The main drawback of this approach is that it is time consuming to setup the joint venture and reach a settlement contract between the neutral operator and banks.

c. Commercial Processor

The commercial processor approach is the same as the neutral operator approach, except that a commercial entity manages the routing, clearing and settlement of transactions. Compared to the previous approach, the commercial processor adds a cost layer on the transactions.

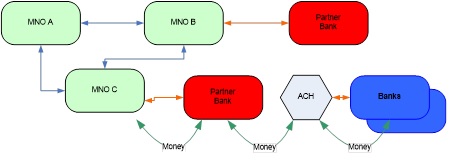

d. Partner Bank to national automated clearing house (ACH)

This option is a variation of option a. MNOs interconnect directly with each other but rely on a partner bank for bank-side settlement. The partner bank is a member of the ACH. The only ACH in Mauritius is the Port Louis Automated Clearing House (PLACH) owned and operated by the Bank of Mauritius.

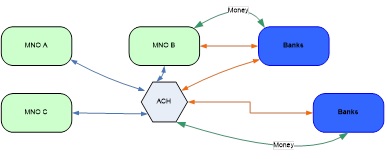

e. Direct Connectivity to a national ACH

In this option, mobile payment schemes connect directly to the national ACH and submit transactions directly to it without using a partner bank. This setup allows all transactions, including inter-scheme transactions to be handled by the ACH. The ACH needs in turn to allow references for mobile wallet accounts as well as bank accounts. This is rendered possible by a Switch which also handles the routing segment. This approach will provide MNO schemes a fast track access to reach all banks, and is envisaged part of the National Payment Switch project of the Bank of Mauritius.

Preferred option

The proposed integration and interoperability model must take into account:

a) the existing payment schemes;

b) the payment models which are either bank account linked or wallets;

c) reach all banks and MNOs;

d) extensible to new entrants in the market;

e) fast and secured settlement

In this contact, option e described above is preferred. It is also preferred that the Mobile Payment Switch operates in the first instance within the Bank of Mauritius and implemented in such a way that it later integrated the National Payment Switch without any additional cost.